India's Exports Decline in January, Trade Deficit Widens

India's exports fell for the third straight month in January, while the trade deficit widened to USD 22.99 billion. Gold imports rose, but crude oil imports fell.

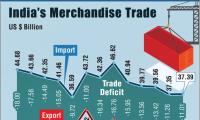

New Delhi, Feb 17 (PTI) India's exports declined for the third month in a row in January, falling by 2.38 per cent year-on-year to USD 36.43 billion, while the trade deficit widened to USD 22.99 billion in the month.

Imports rose by 10.28 per cent year-on-year to USD 59.42 billion in January due to an increase gold shipments, according to the Commerce Ministry data.

The trade deficit was USD 21.94 billion in December and USD 16.55 billion in January last year.

Commerce Secretary Sunil Barthwal told reporters that despite economic uncertainties in the world, India's exports are doing better in both goods and services sectors.

He said that sectors like electronics, pharma, rice and gems and jewellery are registering health growth rates during the month under review.

"Despite conflicts, and tariff retaliation around the world, we are doing well," Barthwal said, adding India's goods and services exports would cross USD 800 billion in 2025-25.

Total exports were worth USD 778 billion in 2023-24.

In January, gold imports rose to USD 2.68 billion from USD 1.9 billion in the same month last year. Gold imports were USD 4.7 billion in December 2024.

Crude oil imports fell to USD 13.43 billion from USD 16.56 billion in January 2024 and USD 15.27 billion in December 2024.

The data showed that the estimated value of services exports for January 2025 was USD 38.55 billion compared to USD 31.01 billion in January 2024. Imports, on the other hand, are estimated at USD 18.22 billion compared to USD 14.84 billion in January 2024.

On the goods front, key export sectors, including petroleum, and chemicals, have registered negative growth during the month under review.

Petroleum product shipments declined by 58.66 per cent to USD 3.56 billion last month. However, textiles, electronics, engineering, rice and marine products recorded healthy growth in January this year.

Cumulatively, during April-January this fiscal, exports rose by 1.39 per cent to USD 358.91 billion and imports by 7.43 per cent to USD 601.9 billion.

Trade deficit, the difference between imports and exports, during the ten-month period widened to USD 242.99 billion. During the first ten months of this fiscal, petroleum product exports contracted by 24.76 per cent year-on-year to USD 53.06 billion.

Commenting on the data, Federation of Indian Export Organisations (FIEO) President Ashwani Kumar said the decline can be attributed to the volatility in commodity and metal prices, as well as ongoing trade disruptions such as the tariff war and currency fluctuations.

Kumar however said this surge in imports, coupled with the widening trade deficit, has raised alarms about potential impacts on domestic industries and the overall trade balance.

"The depreciating value of the Indian rupee, which has fallen by 1.4 per cent against the US dollar since the beginning of the year, further exacerbates the nation's trade challenges," he said adding the depreciation has contributed to higher import bills, especially since India meets 90 per cent of its oil demand from overseas.

Imports rose by 10.28 per cent year-on-year to USD 59.42 billion in January due to an increase gold shipments, according to the Commerce Ministry data.

The trade deficit was USD 21.94 billion in December and USD 16.55 billion in January last year.

Commerce Secretary Sunil Barthwal told reporters that despite economic uncertainties in the world, India's exports are doing better in both goods and services sectors.

He said that sectors like electronics, pharma, rice and gems and jewellery are registering health growth rates during the month under review.

"Despite conflicts, and tariff retaliation around the world, we are doing well," Barthwal said, adding India's goods and services exports would cross USD 800 billion in 2025-25.

Total exports were worth USD 778 billion in 2023-24.

In January, gold imports rose to USD 2.68 billion from USD 1.9 billion in the same month last year. Gold imports were USD 4.7 billion in December 2024.

Crude oil imports fell to USD 13.43 billion from USD 16.56 billion in January 2024 and USD 15.27 billion in December 2024.

The data showed that the estimated value of services exports for January 2025 was USD 38.55 billion compared to USD 31.01 billion in January 2024. Imports, on the other hand, are estimated at USD 18.22 billion compared to USD 14.84 billion in January 2024.

On the goods front, key export sectors, including petroleum, and chemicals, have registered negative growth during the month under review.

Petroleum product shipments declined by 58.66 per cent to USD 3.56 billion last month. However, textiles, electronics, engineering, rice and marine products recorded healthy growth in January this year.

Cumulatively, during April-January this fiscal, exports rose by 1.39 per cent to USD 358.91 billion and imports by 7.43 per cent to USD 601.9 billion.

Trade deficit, the difference between imports and exports, during the ten-month period widened to USD 242.99 billion. During the first ten months of this fiscal, petroleum product exports contracted by 24.76 per cent year-on-year to USD 53.06 billion.

Commenting on the data, Federation of Indian Export Organisations (FIEO) President Ashwani Kumar said the decline can be attributed to the volatility in commodity and metal prices, as well as ongoing trade disruptions such as the tariff war and currency fluctuations.

Kumar however said this surge in imports, coupled with the widening trade deficit, has raised alarms about potential impacts on domestic industries and the overall trade balance.

"The depreciating value of the Indian rupee, which has fallen by 1.4 per cent against the US dollar since the beginning of the year, further exacerbates the nation's trade challenges," he said adding the depreciation has contributed to higher import bills, especially since India meets 90 per cent of its oil demand from overseas.

You May Like To Read

MORE NEWS

© 2025 Rediff.com India Limited. All rights reserved. Disclaimer - Terms of Service - Privacy Policy - Feedback

© 2025 Rediff.com India Limited. All rights reserved. Disclaimer - Terms of Service - Privacy Policy - Feedback